Q1 2022 Open Sustainability Trends: Green Fintech Potential

11 min read

Share this article

At Platformable, we believe in the importance of sustainability and are dedicated to studying how open banking and open finance allow for greater greentech opportunities. To that end, we've released our first Open Sustainability Trends report, Using Open Banking and Open Finance APIs to Build Green Fintech. In the report, we explain how Europe and the UK use open banking and open finance APIs to enable the growth of new sustainability-focused financial digital products and services.

Impactful green fintech requires action for all ecosystem stakeholders

Green fintech are a subset of digital finance products and services that offer features to address sustainability: they seek to enable action towards reducing, adapting or addressing the impacts of the climate crisis, reduce pollution, improve biodiversity and the sustainable use of natural resources, and/or assist with the move to a circular economy in which the full cost of resource use is considered in economic systems.

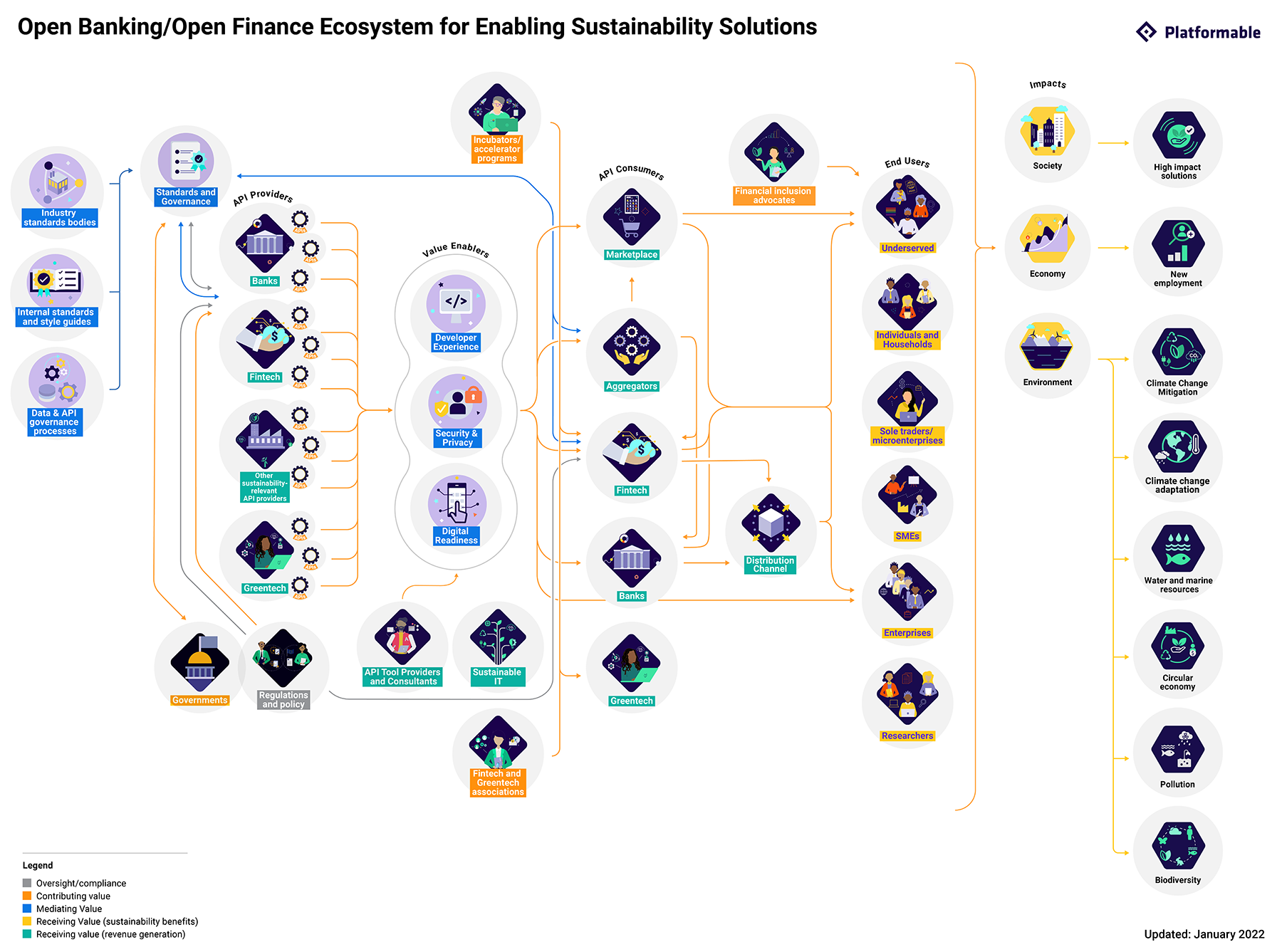

Open banking and open finance infrastructures enable a greater range of stakeholders to participate in the creation and use of financial services through securely exposing application programming interfaces (APIs) as the building blocks for creation of digital products and services.

The value of APIs for sustainability are described in the value model, shown above. From left to right:

- API providers (banks, fintech, and other environmental data providers) make APIs available

- API consumers (fintech, API aggregators, and greentech) use the APIs to build new products and services

- End users (individuals, businesses, enterprises, and researchers) use the products and services, improving sustainability.

All of these actions lead to impacts on society, local economies and the environment.

Other stakeholders (including standards bodies, API tool providers and consultants, incubators, financial inclusion advocates and fintech and greentech associations) all play a part in fostering maturity and furthering the growth of this new industry sub-sector.

Policy and regulation drivers for open sustainability and green fintech

International climate and environmental policy create a global forum for action

The 2015 Paris Agreement set legally binding targets to limit climate change, establishing a target of limiting global warming to 1.5ºC degrees and a need for urgent decarbonisation of the global economy and societies.

Beyond climate change, other global environmental threats are starting to get recognised as having equal importance. The Convention on Biological Diversity is gathering in Kunming, China, in April 2022 to discuss a new global biodiversity framework and to urge global, regional and national policy action to overhaul economic, social and financial models to reverse trends of biodiversity collapse.

The UN Environment Program has proposed a new global digital ecosystem to collect and share data, via APIs, to enable greater collaboration and coordination between stakeholders to address climate and biodiversity impacts.

Regulations: the UK

The UK was the first to legislate a net-zero target in 2008 with the Climate Change Act. The Environmental Act of 2021 has now set additional targets for air and water quality, waste and biodiversity loss. A due diligence requirement for larger businesses was also introduced to require supply chain monitoring in order to address issues related to illegal deforestation globally.

Regulations: EU

European Union member states account for 8% of all global CO2 emissions annually. The EU has committed to becoming the first climate neutral continent by 2050, with a radical reduction in GHG emissions required by 2030. The European Green Deal, widely supported by the European public, is the main strategy for transforming the Union into a modern, resource-efficient and competitive economy. It encompasses a wide range of regulations and directives, including:

- European Climate Law establishes the framework for achieving climate neutrality in the Union by 2050 and a reduction of GHG emissions of at least 55 % compared to 1990 levels by 2030.

- The Non-Financial Reporting Directive (NFRD) requires large, public-interest companies to self-declare their performance related to environmental and social matters. A proposal to expand its scope was adopted in April 2021 and the proposed replacement, Corporate Sustainability Reporting Directive (CSRD) is expected to be adopted during 2022. The CSRD would expand the definition of companies required to report on sustainability performance, introduce a third-party audit requirement, and unify reporting standards. The European Securities and Markets Authority has also released a roadmap for sustainable finance, which prioritises assessment of greenwashing, and identifying innovative use cases, amongst others.

- EU Taxonomy regulation, a classification system for economic activities, includes definitions and rules to determine which economic activities are environmentally sustainable.

- The EU’s digital strategy recognises the enabling nature of digital in accelerating the sustainable transformation through things like improved connectivity and infrastructure and an access to high-quality and interoperable data - examples of setting to spur new product development.

- The Circular Economy Action plan, adopted in 2020, includes 35 actions and initiatives along product life cycles to maximise resource efficiency and improve circularity rates in resource intensive sectors such as electronics, textiles, packaging and construction.

How global, European and UK regulations can drive action

The setting of commitments, and new requirements for businesses and companies to report on Environmental, Social and Governance (ESG) impacts and monitor their supply chains creates new opportunities for fintech and business-focused products that address these regulatory requirements in new digital products. Such regulations also help open up new markets by creating demand and encouraging the development of new solutions that help stakeholders comply with the new regulatory context.

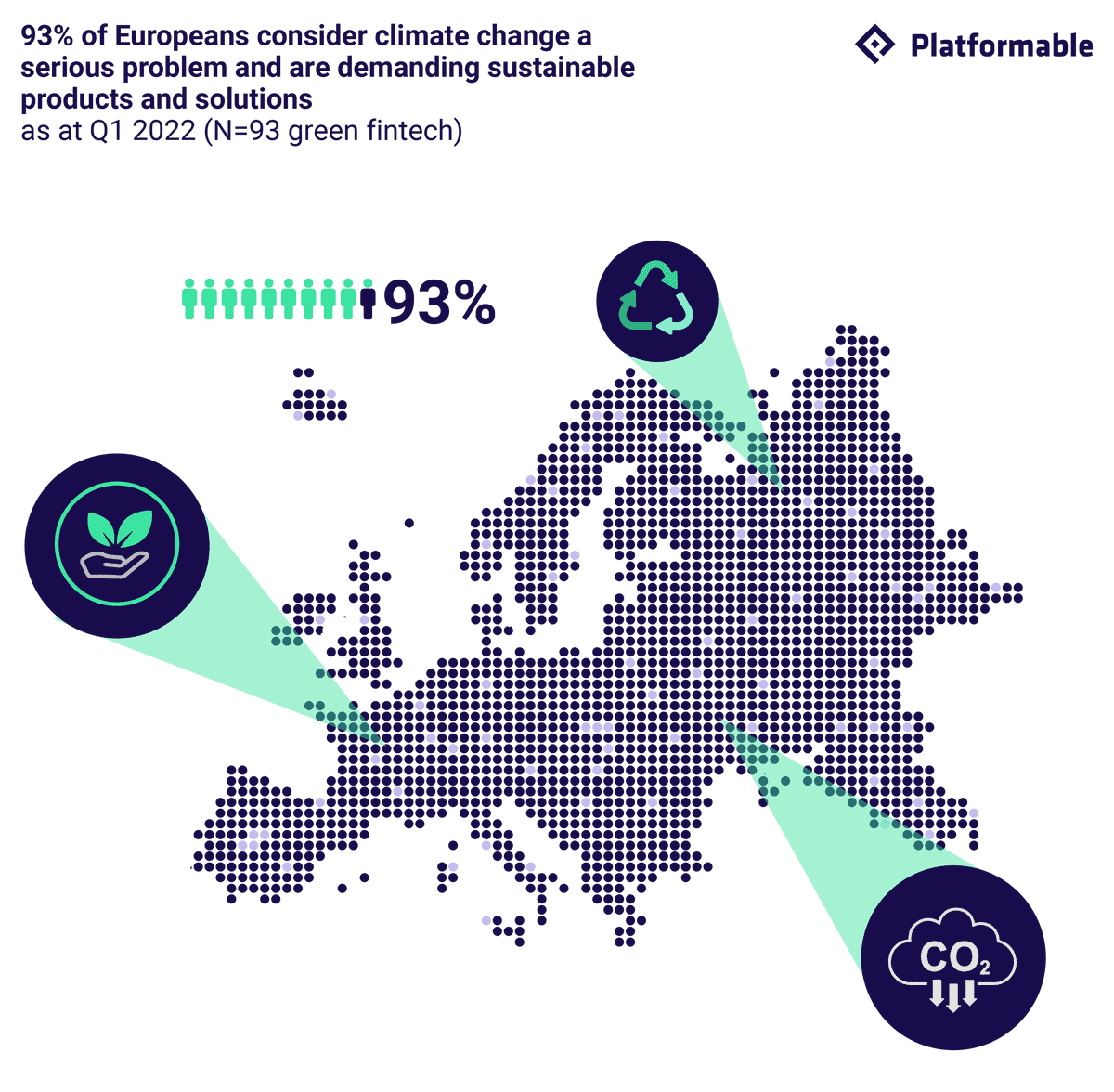

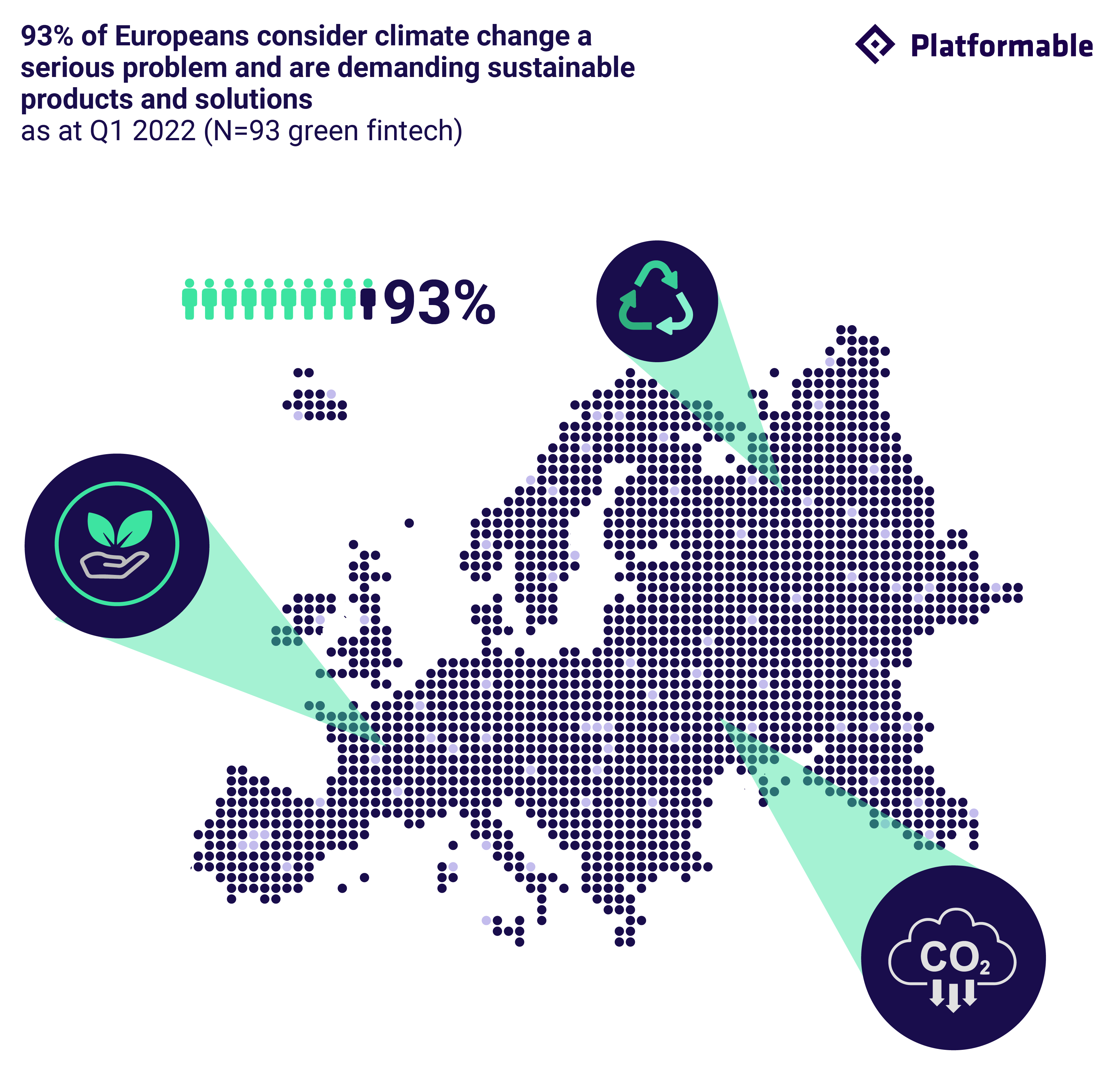

93% of Europeans consider climate change a serious problem and are demanding sustainable products and solutions

Consumers are increasingly demanding more sustainable digital products and services, including in their finance choices. Combining sustainable and digital transformation future-proofs a business and enhances market strength.

Environmental concern and demand for “green” products is high

A 2021 Eurobarometer survey found that 93% of Europeans consider climate change a serious problem. Another survey by YouGov stated that three quarters of Europeans believe that governments can have a big or fairly big impact, while 4 in 5 say businesses play an important role in addressing climate change.

Additionally, a 2021 UK study by Deloitte found that:

- 8% of survey respondents had already changed some or all of their personal finance investments to ethical or sustainability-related options

- 34% of respondents had specifically chosen brands because of their environmentally sustainable practices and values.

Digital and sustainability transformation for business success

Digital transformation has proven essential since the onslaught of the COVID-19 pandemic, with the World Economic Forum noting that 65% of the world’s GDP will be digitised by the end of this year. Businesses coupling sustainability with digital transformation are forecasted to be 2.5 stronger as market performers than businesses that do not align their business processes with sustainability models.

The Green Digital Finance Alliance has commenced a number of initiatives focused on supporting consumer behaviour towards sustainable action via use of fintech solutions:

- The Every Action Counts coalition seeks to empower 1 billion global consumers to take daily actions to support sustainability, partly through greater adoption of green fintech products and services

- The Nordic Energy Efficient Mortgages Hub notes the potential for fintech to overcome current barriers in energy efficiency uptake by consumers, in part by addressing the lack of finance-ready data to support consumer choices.

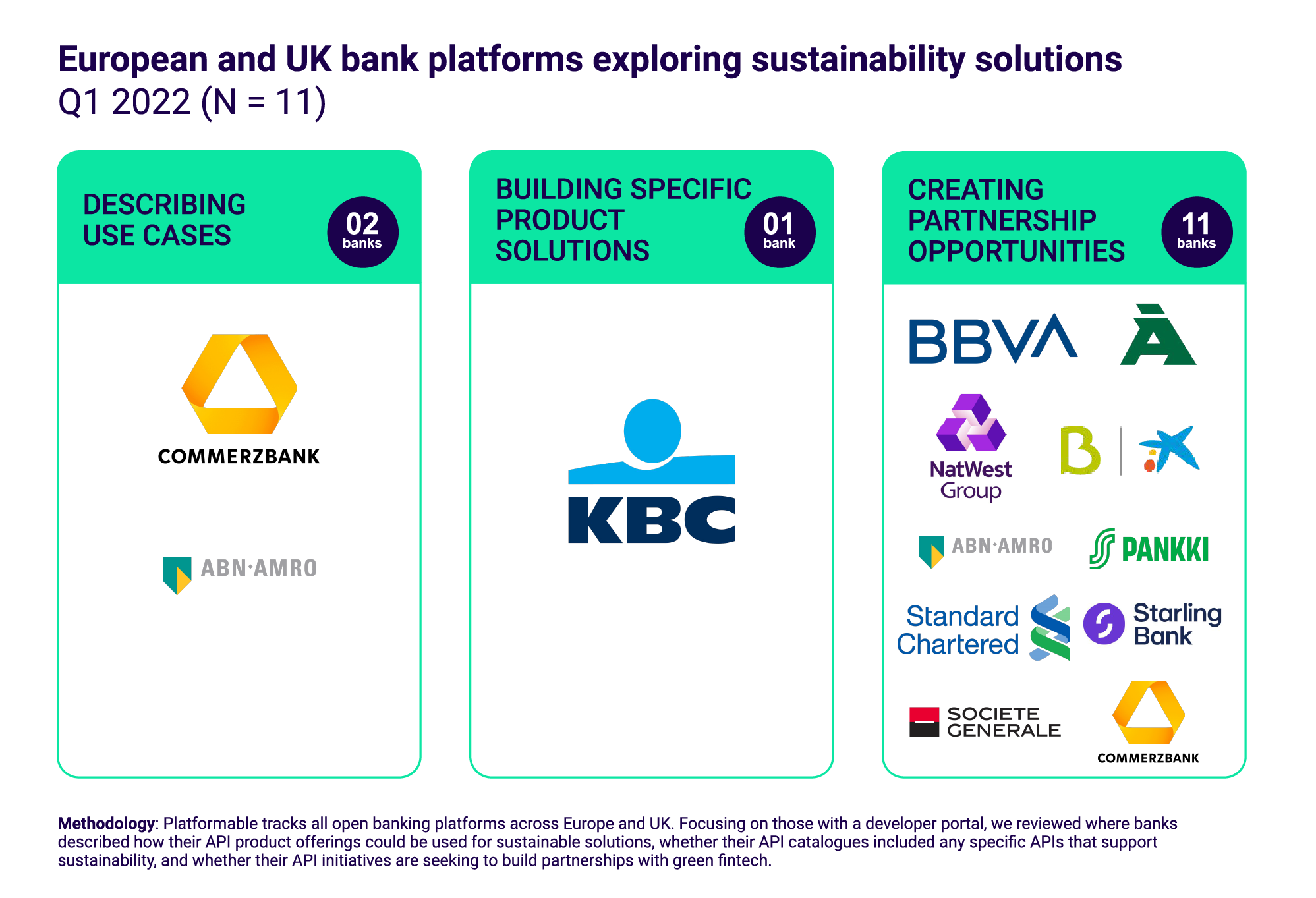

11 European and UK banks explicitly seek climate action opportunities for their API programs

Core open banking API products like PSD2-mandated payments and account information can assist green fintech to start building new digital products and services.

Open banking platforms that seek to support green fintech to build innovative solutions are going beyond mandated APIs in three ways:

- Describing potential sustainability use cases that their existing API functionalities can help build. Commerzbank’s corporate payments API, for instance, has helped Energie Revolt build an energy prepayment solutions for their end- SMEs and enterprise customers.

- Building specific sustainability product offerings. KBC, for example, offers bicycle and green energy loans solutions that allow merchants to offer their end customers credit financing for their purchases at the point of sales, in store or online.

- Creating partnership opportunities where banks work with third parties to explore sustainability solutions (e.g. Standard Chartered). Some banks have opened incubation programs (e.g. ABN Amro, Bankia, Natwest Group) or acquisition tracks (e.g. Societe Generale) to recruit fintech partners for a number of areas, including sustainability solutions. These partners can access the banks’ resources to build and test their products.

Creation of green fintech products requires collaborative action by more stakeholders

To create truly impactful green fintech products will require collaboration amongst a greater range of stakeholders:

- Green APIs expose specific sustainability-focused functionalities or data, and coupled with bank or fintech APIs can allow more innovative products to be built. Energy switching functionalities, carbon accounting algorithms, and ESG data aggregation services are examples of green APIs that can be consumed by fintech to create sustainability impacts.

- Fintech and greentech associations build networks, showcase actions and best practices, promote challenges, and encourage their members to partner on solutions.

- Incubators enable product ideation and fund emerging initiatives. Their role is particularly important in young industries, where a lot of trial and error is required to create business-viable and impactful products and services.

- Accelerators provide business support to the most promising ideas, and enable teams to reach product and scale-up stages. They often operate with direct pipelines to potential VC funding.

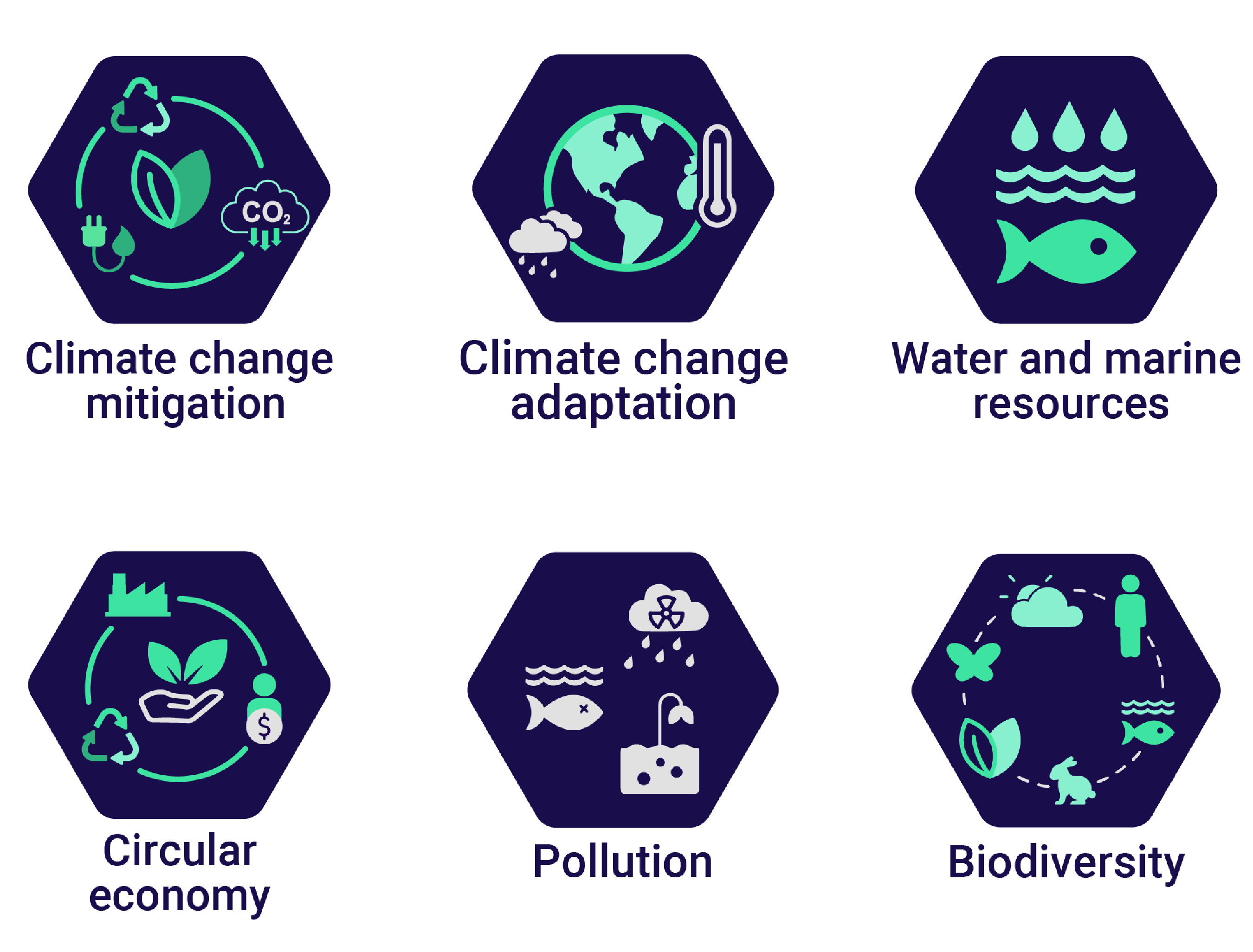

Measuring the impact of green fintech products

There are 6 sustainability impacts, based on the classification from the EU’s six environmental goals:

- Climate change mitigation

- Climate change adaptation

- The sustainable use and protection of water and marine resources

- The transition to a circular economy

- Pollution prevention and control

- The protection and restoration of biodiversity and ecosystems.

These impact categories are used to classify positive sustainability and environmental impacts created with green fintech products and solutions. The model looks at environmental well-being beyond the narrow scope of climate change mitigation and carbon dioxide to include moves towards better management of water and marine resources, generating a circular economy and reducing the risk of biodiversity collapse.

The impact categories are not mutually exclusive but often reinforcing. For example, the ecosystem regeneration service SUGi, increases climate change mitigation by adding forest cover, but also seeks to protect biodiversity and help local communities adapt to climate change.

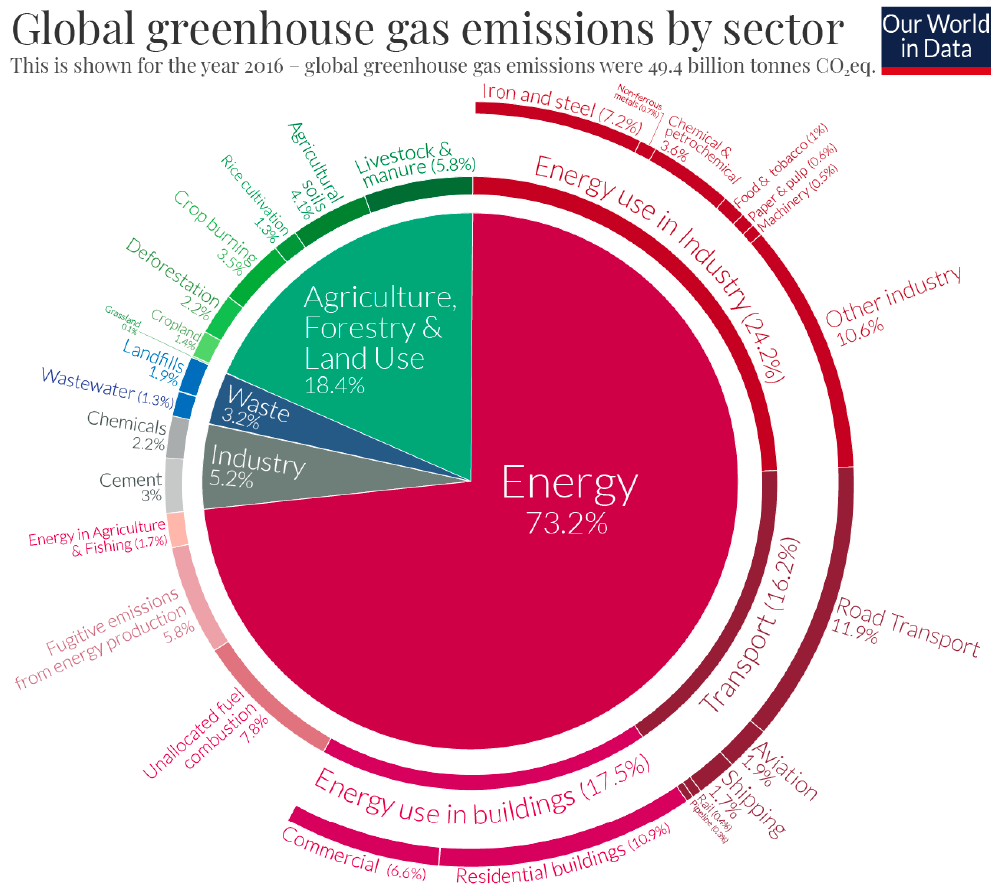

When it comes to climate change mitigation, green fintech solutions must focus on high-impact sectors

Globally, the majority of greenhouse gas emissions come from four high-impact sectors:

- Energy use in industry

- Transport

- Energy use in buildings

- Agriculture and land use change

In order to deliver the ambitious emissions reductions needed, these sectors should be the main focus of sustainability solutions.

To generate the greatest sustainability impacts, emerging green fintech — and existing fintech adding new sustainability features to products — will need to focus on these key areas.

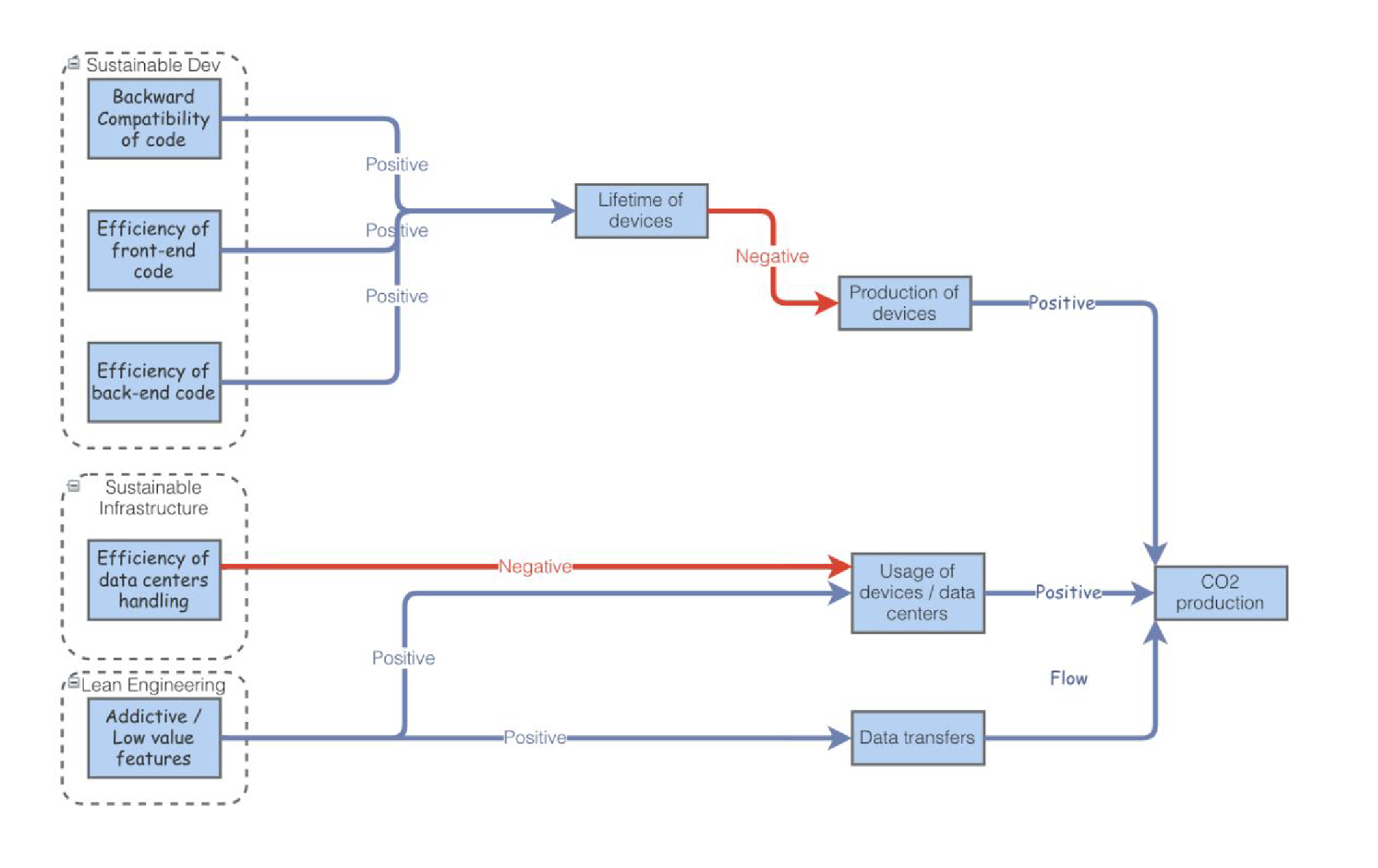

Green fintech needs to be built on sustainable IT practices

Source: apidays Sustainable Digital Report 2021, downloadable from apidays

While open banking and open finance APIs can support the development of new digital products and services focused on improving sustainability, they will make greatest impact if the underlying technology infrastructures themselves are energy efficient and sustainable.

A white paper on green cloud software practices, published openly in January 2022, and led by tech ethicist Anne Currie, (and discussed by tech journalist Jennifer Riggins in The New Stack), outlines key priorities for action to ensure that the IT infrastructure offering sustainable solutions is itself sustainable. The authors note the main approaches for reducing carbon emissions from software products (in order of effectiveness) are:

- Operational efficiency (i.e. improving how software is run)

- Architecting for minimal carbon (improving how software is designed)

- Hardware efficiency (in particular, improving how end user devices are managed)

- Energy efficiency (minimizing CPU/GPU and network use).

To address operational efficiency, the apidays Sustainable Digital Report 2021 describes how designing and writing efficient code, including in API design and delivery, can improve sustainability.

Interested in learning more about sustainability in the open bank and open finance sectors?