Analysis: 3 banks (1.5% of all banks with APIs) are leveraging their API platforms for COVID-19

12 min read

Platformable’s Open Banking Quarterly Trends Report seeks to monitor the transition to open banking economies, in which bank services are available via APIs so that third parties (especially fintech) are able to create new products and services.

In Q1 2020, we observed 2 banks that have specifically used their open banking API infrastructure to address COVID-19 impacts of consumers. We have since heard of 1 other bank that has worked with restaurants to assist them use payments APIs and move to online payment models. Therefore, in total, our data shows that only 3 banks out of 197 (or 1.5%) are leveraging their open APIs to address COVID-19.

Context: The impact of open banking regulations

In some countries, new regulations are insisting that banks open APIs in order to ensure greater interoperability, to allow greater consumer control over financial data, to enhance competition, and/or to diversify the range of products available to consumers. In other countries, banks themselves see the potential of creating a platform approach, and are opening APIs and integrating with new partners.

One of the expected benefits of opening APIs is that fintech are able to create new products and services, and to date, consumers appear to be willing to move some of their financial operations to new fintech and to challenger banks in order to access more niche products and apps that offer an engaging user experience (UX). At times like now, with the COVID-19 pandemic impacting every aspect of our lives and societies, consumers are often more inclined to behave more conservatively and to return to more traditional institutions. In some quarters, fintech are seeing a downturn and the zest amongst consumers for moving to challenger banks is more muted. In other cases, there is still a lot of movement and investment occurring amongst API-enabled fintech.

Bank priorities in the age of COVID-19

Our Open Banking Quarterly Trends Report was unable to measure the full impact of COVID-19. This is partly because only one month of data was affected (March 2020): we expect our Q2 report to have a more comprehensive view. But even one month in, key characteristics were emerging:

- Banks are more focused on their core business and customers

- Open banking APIs are not seen as an opportunity to support customers during times of crisis

- Banks are beginning to turn to API teams to assist with digital transformation more widely

- Fintech are more readily building new COVID-19 products.

Banks are more focused on their core business and customers

Key informants from banks that we spoke to during the Quarterly Trends Report data collection process pointed to three key reasons why banks were not leveraging their open APIs:

- They are focused on supporting their staff transition to remote work

- Their call centres are overwhelmed and they are focusing their efforts on managing a sharp increase in core customer engagement

- In some cases, banks are seeing new regulations, such as government insistence that banks allow customers to pause their loans, and so banks are working to address the new business logic and financial impacts that are involved in implementing these requirements.

Open banking APIs are not seen as an opportunity to support customers during times of crisis

Open banking APIs are still in their nascency and so for many open banking teams, the killer use cases and business model opportunities have not yet emerged. Some banks were not yet seeing sufficient compelling use cases of third parties integrating their APIs. So they did not see a priority in further investing in their open API infrastructure to support fintech create new products that address COVID needs.

Banks are beginning to turn to API teams to assist with digital transformation more widely

While some banks we spoke to indicated they had C-level sponsorship for their open API programs, others mentioned that the wider IT banking infrastructure teams were now asking them for help in establishing governance and style guidelines for creating internal APIs. We expect to see this become more common during Q2, as banks shift their staff and organisational structures towards enabling digital transformation sooner than previously planned.

Fintech are more readily building new COVID-19 products

Despite the bank point of view, fintechs are building new COVID-19 related products and services. Many businesses are already challenged by cashflow droughts and fintech are seeking to create new products and services for these businesses in ways that banks are not. Fintech have also quickly introduced new products to assist in instant payment transfers so that community members can support each other.

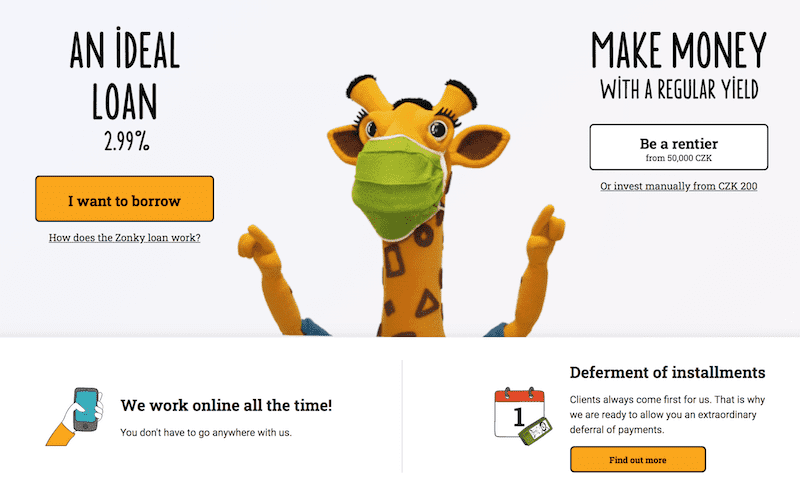

Zonky, accredited in the Czech Republic, continues to offer crowdfunded loans and have now added a payment deferral system in line with government laws to ensure loan customers can maintain their loans over the longer term. (They also updated their website to show their mascot wearing a face mask.)

Personal Financial Management app Spendee (accredited in 25 countries across Europe) shared some data on spending habits under COVID-19. You can see a use case where they partner with banks and other fintech to better understand sales data for businesses that are most at risk and identify those that may require additional support.

Spanish-based Fintonic (which is accredited under PSD2 in 31 jurisdictions across greater Europe and the UK) offers bank and other loans. Like Spendee, they have identified current financial impacts for individuals and households that may be useful in identifying customer segments in need of additional financial services.

UK-based and accredited Ordo originally sought fintech accreditation to target small business customers but appear to have pivoted slightly to create a P2P transfer app to support neighbours buying food for those isolated or vulnerable and unable to shop during the pandemic.

Where banks and fintech are heading

In Q2 we expect to see:

- Fintech more acutely messaging their COVID-19 product offerings in order to differentiate from banks further, and even abandoning bank APIs in favour of payments infrastructure APIs to create products for the market

- Banks increasingly co-opting their open API teams to work on internal API infrastructure

- Consumers outside the core customer base of banks will increasingly be left to fend for themselves.

The biggest worry we see is that as banks strengthen their focus on core customers and on their traditional product offerings, they may de-prioritise supporting niche customer segments with particular needs. Given that customers act more conservatively in a crisis, we understand this focus. But banks were left behind in the fintech revolution because they weren’t willing to diversify and offer customers more niche products aimed at particular consumer needs. Open banking is meant to break down the antiquated, conservative model of generic financial services products. If banks are not able to support marginal customers, they should be using their open API platforms to encourage others stakeholders (fintech) to meet those edge customers’ needs. Possible customer segments could include:

- Adult households that need to care for ageing parents

- Families that need to invest in more educational resources

- Health care workers who are eligible for hazard pay and other subsidies

- Remote workers who need to purchase equipment to transition to setting up a home-based office

- Small businesses and freelance/independent workers that may need access to lines of credit, factoring, or other cashflow services that help them better manage cashflow over three to six months rather than one to two months.

If banks are unable to support these types of customer needs, they should partner with fintech to create products and services that do address these challenges. Given that banks are currently overwhelmed with the above-described internal systemic issues, that could at least make it easier for fintech to build using their APIs.

Banks could also follow JPMorgan’s model and work with governments to facilitate more seamless stimulus and financial support models. (We're curious to see if the Canadian and Berlin systems, in which citizens received their financial stimulus payments almost overnight, were able to do so because of government use of APIs: we will followup on this in a later post.)

A non-exhaustive list of what open banking stakeholders could focus on

What banks could do:

- API teams within banks would do well to document the benefits of open banking (sharing metrics on new account creation and increased transaction volume enabled through open APIs, for example). Teams should also get their documentation in order and build out their centre of excellence training resources so that they are ready when core IT teams and lines of business come knocking and ask for help. It will also be important for API teams to show their flexibility and assist lines of business to achieve the line of business goals. That is, API teams should seek to understand rather than be understood.

- Identify segments outside your core customers that face specific needs. ABN AMRO and DBS Singapore for example both identified that restaurants needed help to integrate payment APIs so that they could transition to online ordering and mobile payments systems. A key concern at present is that independent retail is down, but Amazon ecommerce is way up. Banks supporting business models like Bookshop.org (in the United States) could help ensure that independent retail (for any vertical) has a greater chance of surviving through this pandemic.

- Create a banner on your API portal to highlight that your APIs can be used to build new fintech products to address COVID-19 impacts. Most banks have core messaging on their customer portals. Link to that content and show how that messaging flows through to API partnerships. Write a specific blog post describing some of the identified customer segments that could benefit from fintech products.

- Consider offering some incentive to fintech to use your bank APIs: perhaps some individual mentoring or pair programming to speed up onboarding would be helpful. Or co-marketing/showcasing of any products built by fintech. If there is a pricing model for your APIs, perhaps you could offer discounts for fintech building products for COVID.

- Our one pitch: Contact Platformable for a list of fintech accredited in your region with the potential to address your identified customer segments. We can also help identify interesting use cases that match your identified segment needs.

What fintech could do:

- Identify customer segments requiring additional support.

- Look for bank partnerships where your product idea is not in direct competition with the bank’s product range.

- Reach out to fintech associations and work together to advocate for fintech’s role in connecting government stimulus packages with end customers.

What consumer advocates could do:

- Help document and describe those at greatest risks from COVID impacts. For example, in the United States, up to 90% of women and minority-owned businesses were shut out from receiving business support loans from government. In Europe and the UK, healthcare workers may be eligible for additional financial supports and many of these are migrant workers who need to share their finances with families in their country of origin.

- Work with fintech and banking associations to ensure APIs can be used to integrate and automate stimulus payments so that those in need receive their finances in a timely manner.

What the API industry could do:

- Create content showing your value in assisting banks and fintech to partner and work together to build products using APIs.

- Monitor examples of successful fintech products built with bank APIs and see how your tooling could help support and maintain the performance and security of those apps. (For example, as shown below, 10 messaging/communication platform/chatbot API tool providers currently have bank clients. Banks and fintech would seem a particular market well suited to targeting at present by these providers as banks have described greater workloads in their call centres during COVID-19.)

What we can expect in the open banking economy in Q2 2020

There are still opportunities available to banks to reorient themselves towards open banking and to work in partnership approaches to create innovative products to assist consumers. And while we only identified three that publicly have leveraged their banking APIs to address COVID-19 financial impacts, we do regularly speak with other banking stakeholders that have discussed a keen interest in partnering with fintech to create new services that manage the financial challenges and sudden jolts that COVID-19 is causing on individual, household and small business finances. But banks need to do more. The landscape is changing rapidly and a key risk of COVID-19 is that it will squeeze out small and medium businesses in favour of the tech giants. If that happens, banks lose as well, as those tech giants are a much greater direct competition threat than the UX-focused fintech providers that banks could partner with.

It is unclear if banks appreciate that risk or are willing to make further efforts to support their customers during COVID-19. My own bank, based in Spain and which I chose specifically because of their leadership with APIs, does not make some of the government-subsidised loan packages available to their customers directly. Their bank customers seeking rental relief, for example, must go through government application processes rather than via the bank. This is a missed opportunity to rebuild the trust that fintech are taking from banks and isolates banks as unconcerned with their customers financial health and wellbeing.

Even amongst banks that are more innovative, movement can be slow. Several large banks have announced major employment cuts during COVID-19, which will further erode traditional branch and banking infrastructure and allow banks to speed up their digital transformation efforts by reorienting towards IT flexibility and digital service delivery. That will be a huge task in itself. (Again, banks would do well to invest further in API teams to both foster third party partnerships and also ensure that internal API expertise can also play a role in this structural reorientation.)

The missing voice in all of this so far has been the consumer associations. To date, there has been little advocacy from consumer representatives arguing for greater digital service delivery for those most impacted by COVID-19. In Q2 and into Q3, we hope to see greater collaboration and leadership from consumer representatives arguing for the use of API technologies to more quickly build the needed financial health products.

Moreso than regulations, COVID-19 may end up shaping the future of open banking. Q2 and Q3 this year will make clear what direction open banking is headed towards, but for now, there is plenty of partnership work to do.